Reverse mortgages have become a popular topic in New Zealand due to several factors. The country’s aging population, coupled with historically high house price growth, means that many older Kiwis are considering reverse mortgages as a means of accessing the equity in their homes and turning it into cash. However, the question remains: are reverse mortgages a sound retirement strategy?

What is a reverse mortgage?

A reverse mortgage is a financial product available to homeowners in New Zealand. Essentially, it is a loan where you borrow money against the value of your property. The loan is repaid when you sell your house or when you pass away.

The amount you can borrow will depend on your age and the value of your home. Typically, you can borrow between 15-40% of your home’s current value. The loan will accumulate interest over time, and New Zealand reverse mortgage providers currently offer interest rates around 8-9%.

Benefits of a reverse mortgage

One of the key benefits of a reverse mortgage is that you can use the money for any purpose you choose. This can include home repairs, health care, holidays, a new car, or even as an income top-up. You can choose to receive the money as a lump sum or in regular instalments.

One of the most attractive features of a reverse mortgage is that you don’t need to make repayments until your home is sold. This can be especially appealing for retirees who may be living on a fixed income. Additionally, some lenders offer guarantees that you will never go into negative equity, meaning that even if the loan balance exceeds your home value, you or your estate cannot be chased for the difference.

As house prices increase over time, the equity in your home increases and reduces the overall loss in equity when it comes to sell the home.

Considering a reverse mortgage for retirement?

Our mortgage advisors help retirees and homeowners access property equity safely, so you can boost income or cover expenses without stress.

Talk to a mortgage adviser today

Expert guidance from a trusted mortgage broker

Understand reverse mortgage options and terms

Tailored advice to protect your home and retirement

Things to look out for

However, there are some downsides to consider. Firstly, not all properties are eligible for reverse mortgages. Some lenders may not offer reverse mortgages on larger properties such as lifestyle blocks and farms, or properties with problematic building materials. Additionally, if you want to rent out your property or move into a care facility, you will need to sell your home and repay the loan.

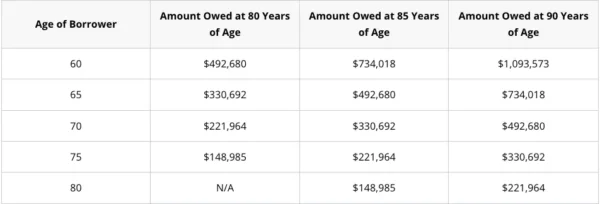

Another important consideration is that lenders charge higher interest rates on reverse mortgages than traditional mortgages. This is because the loan is usually not repaid for a long period of time, and interest compounds monthly. This means that loans of $100,000 can quickly balloon to over $490,000 over 20 years.

In the table below, MoneyHub shows how much debt a $100,000 loan (with an 8% p.a. interest rate) can create.

4 essential terms and conditions

- Firstly, if you are a couple, it is essential for both of your names to be on the mortgage contract. This means that if one of you passes away or moves into care, your home will continue to be in the possession of the other person.

- Secondly, make sure the mortgage contract allows for ‘lifetime occupancy’. This means that the bank cannot sell it for any reason other than your death or your need to permanently move out.

- Make sure the contract prohibits ‘negative equity’.

- Lastly, make sure the contract has a ‘loan repayment guarantee’ which means you never have to make any repayments until either you pass away or sell your home

For a no obligation discussion to see how we can help you on the path to wealth, please contact us.

Disclaimer:

The information in this article is general information only, is provided free of charge and does not constitute professional advice. We try to keep the information up to date. However, to the fullest extent permitted by law, we disclaim all warranties, express or implied, in relation to this article – including (without limitation) warranties as to accuracy, completeness and fitness for any particular purpose. Please seek independent advice before acting on any information in this article.