A practical look at how investment property loans are commonly structured in New Zealand, and why interest-only lending is widely used by investors.

Property Selection And Finance Structure Work Together

Choosing the right investment property is one of the most important parts of building a successful portfolio.

Location, rental demand, long-term growth potential, cashflow, and property type all influence how an investment performs over time.

But even a strong property can feel difficult to hold if the lending structure is not aligned properly.

This is where finance structure becomes important.

The type of loan attached to an investment property can materially change cashflow, borrowing capacity, and portfolio flexibility. In many cases, the same property can produce very different financial outcomes depending on how the lending is structured.

This is why experienced investors usually look at both the property and the finance strategy together, rather than treating them as separate decisions.

Not all loan types work the same way, and different structures can suit different investment goals.

The Two Main Loan Types Investors Use

In New Zealand, investment property lending generally falls into two broad categories:

• Principal and Interest (P&I)

• Interest-Only (IO)

With a principal and interest loan, repayments cover both the interest cost and repayment of the actual loan balance. Over time, the debt gradually reduces.

With an interest-only loan, repayments only cover the interest being charged by the bank. The loan balance itself generally remains unchanged during the interest-only period.

Both structures are common. The difference is usually less about “right” or “wrong”, and more about what the investor is trying to achieve.

Why Interest-Only Lending Is So Common

Interest-only lending is widely used in property investment because it typically reduces holding costs in the short term.

Since the investor is not paying down principal, the required repayments are usually lower compared to a principal and interest loan on the same property.

For investors, this can improve cashflow significantly.

That matters because many investment properties are negatively geared. Lower repayments can make the property easier to hold while rents and property values potentially increase over time.

For new build investors especially, interest-only lending is often used as a way to improve affordability and portfolio flexibility.

This is also one reason some investors are able to service multiple properties over time. Lower repayment requirements can improve borrowing capacity compared to aggressively paying down debt across every property.

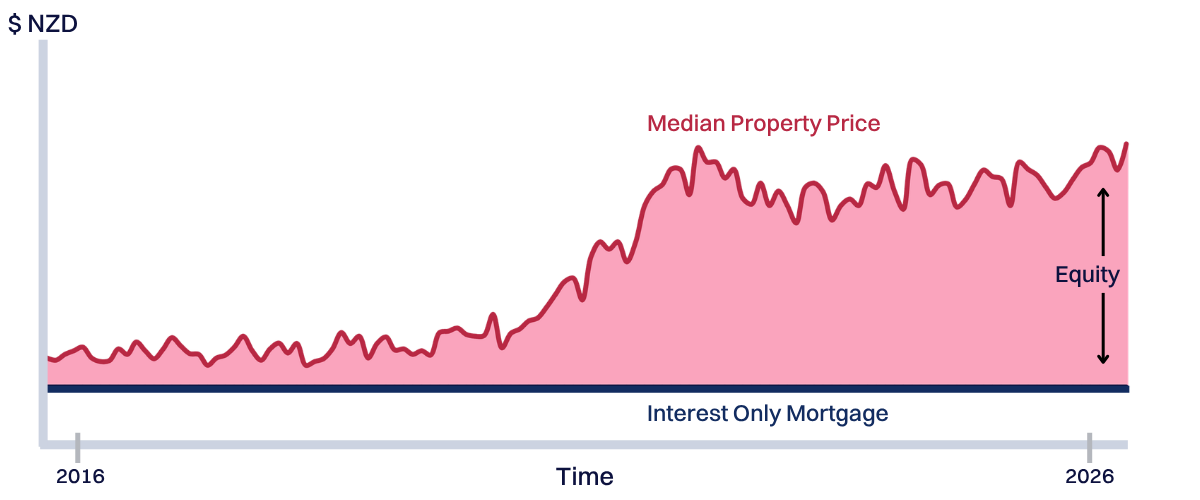

How Investors Actually Build Equity

One of the biggest misconceptions around interest-only lending is that investors are “not building wealth” because the loan balance is not reducing.

But for many investors, the strategy is based more on asset growth than debt reduction.

If a property increases in value over time, the investor’s equity position can still improve significantly, even if the loan itself remains largely unchanged.

That is the key idea behind leverage in property investing.

For example, if a property worth $800,000 increases by 5%, that is a $40,000 increase in value regardless of whether the investor paid down large amounts of principal during that period.

The strategy relies on the property growing in value over time while the debt remains relatively stable.

Principal And Interest Still Has Advantages

While interest-only lending is common, principal and interest lending still has clear advantages.

Because debt is gradually being reduced, investors build equity through repayments as well as property growth.

Over time, this can improve financial security and reduce long-term interest costs.

Principal and interest lending may also suit investors who prioritise debt reduction, lower long-term leverage, or eventual passive income goals.

The trade-off is usually cashflow.

Higher repayments can place more pressure on monthly finances and may reduce borrowing capacity for future purchases.

This is why some investors use different loan structures for different stages of investing.

Loan Structure Often Depends On Strategy

The “best” loan type usually depends on what the investor is trying to achieve.

An investor focused on long-term portfolio growth may prioritise lower holding costs and flexibility through interest-only lending.

Another investor nearing retirement may prefer principal reduction and lower long-term debt exposure.

Some investors also split lending across different structures, combining both principal and interest and interest-only lending within the same portfolio.

The important point is that loan structure is not just a banking decision. It is part of the broader investment strategy.

Cashflow, risk tolerance, income stability, and long-term goals all influence which structure may be appropriate.

The Trade-Offs Still Matter

Interest-only lending can improve cashflow and portfolio flexibility, but it does come with trade-offs.

Because the principal is not reducing, investors generally pay more interest over the life of the loan compared to paying principal down earlier.

The strategy also relies heavily on being able to comfortably hold the property over time.

If property values stagnate or interest rates rise significantly, highly leveraged investors can come under pressure.

This is why buffers, servicing capacity, and risk management remain extremely important regardless of loan type.

A strong investment strategy is not just about buying a good property. It is about structuring it in a way that is sustainable long term

The Structure Behind The Property Matters

One of the biggest shifts experienced investors make is realising that property investing is not just about choosing the right property.

The finance structure underneath the investment matters as well.

Loan type influences cashflow, servicing, portfolio growth, and how manageable the investment feels over time.

Interest-only lending has become common because it can improve flexibility and reduce holding costs, particularly during growth-focused stages of investing.

But finance is only one part of the equation. Choosing the right investment property, one that aligns with your cashflow, risk tolerance, and long-term financial goals, is just as important.

If you want to understand what is best for your situation, feel free to get in touch with the Lighthouse Property Team.

If you’d like to learn more, check out the latest property episode on Cheques & Balances.

Disclaimer:

The information in this article is general information only, is provided free of charge and does not constitute professional advice. We try to keep the information up to date. However, to the fullest extent permitted by law, we disclaim all warranties, express or implied, in relation to this article – including (without limitation) warranties as to accuracy, completeness and fitness for any particular purpose. Please seek independent advice before acting on any information in this article.