A look at how population growth, affordability and local conditions are shaping housing market movements across New Zealand.

Migration and Housing Demand

New Zealand’s housing market is often discussed as if it moves in a single national cycle. In reality, the picture is far more nuanced. While national averages provide a useful overview, housing markets across the country often respond differently to the same economic conditions.

According to the latest data from the Real Estate Institute of New Zealand (REINZ), the national median house price reached $753,106 in January 2026, up 0.4% year on year, suggesting prices have broadly stabilised following the volatility of recent years.

However, beneath the national figure are important regional differences. One of the most commonly cited drivers of housing demand is population growth, particularly net migration.

When migration increases, more households require accommodation. In the short term, housing supply tends to remain relatively fixed because new construction takes time. This can increase demand in both rental and property markets.

How Migration Influences the Housing Market

Migration can influence housing markets through several channels, one of which often begins in the rental sector.

As more people move into an area, the number of households requiring accommodation increases. In the short term, housing supply typically adjusts slowly, which can lead to higher demand for rental properties.

Stronger rental demand can push rents higher, improving rental yields for property investors. Higher yields can make residential property investment more attractive relative to other assets, potentially increasing investor interest in purchasing property.

As investment demand rises, this additional purchasing activity can place upward pressure on property prices over time.

However, this is only one pathway through which migration can affect housing markets. Population growth can also increase demand from owner-occupiers and first-home buyers, meaning migration can influence property prices through several forms of housing demand, not just investor activity.

The Role of Affordability

While population growth can increase overall housing demand, affordability often determines how different markets respond to economic changes.

The period between 2022 and 2023 provides a clear example. During this time the Reserve Bank increased the Official Cash Rate significantly in response to inflation. Higher interest rates reduced borrowing capacity across the housing market, making it more difficult for many buyers to finance property purchases.

When borrowing capacity declines, housing demand often softens, which can place downward pressure on property prices. However, the impact is not always the same across all markets.

Housing affordability is commonly measured by comparing house prices with household incomes. This measure can help explain how sensitive different regions are to changes in borrowing costs.

Auckland and Christchurch: A Comparison in Affordability

Auckland and Christchurch provide an interesting comparison in this context.

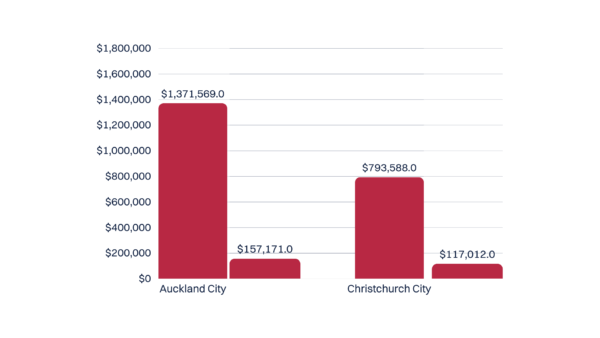

The chart above compares median house prices with median household incomes in both cities.

The chart above compares median house prices with median household incomes in both cities.

Based on this comparison:

• Auckland homes cost approximately 8.7 times the median household income

• Christchurch homes cost approximately 6.8 times household income

Although household incomes between the two cities are relatively similar, the difference in property prices results in a notable affordability gap.

Why Affordability Matters for Market Movements

When interest rates increased between 2022 and 2023, borrowing capacity declined across the country. Markets where prices were already higher relative to income tended to feel the effects of reduced borrowing capacity more quickly.

In contrast, markets where housing remained more affordable, relative to incomes, generally had slightly more flexibility for buyers to absorb higher mortgage costs.

This dynamic may help explain why different regions experienced varying degrees of price adjustment during the recent interest rate cycle.

Importantly, both Auckland and Christchurch remain key housing markets in New Zealand. Auckland continues to be the country’s largest economic centre with strong long term population growth and employment opportunities. Christchurch offers relatively more affordable housing alongside the scale and infrastructure of a major city.

Regional Market Trends

Looking across the country, the REINZ data highlights how regional housing markets can move at different speeds.

Several regions recorded annual median price growth (Jan25-26), including:

• West Coast (+9.3%)

• Otago (+6.7%)

• Southland (+5.7%)

• Canterbury (+3.4%)

At the same time, some regions experienced price declines (Jan25-26), including:

• Northland (-12.5%)

• Gisborne (-13.7%)

• Bay of Plenty (-4.8%)

These differences illustrate how local conditions such as affordability, population movement, housing supply and employment opportunities can influence housing markets differently across the country.

Understanding the Bigger Picture

Housing markets are shaped by a range of economic forces. Migration can influence long term demand, interest rates affect borrowing capacity, and affordability plays a role in how different markets respond to changing conditions.

While national price movements may appear relatively stable, the data shows that regional housing markets continue to respond to these factors in different ways.

Understanding these dynamics helps explain why New Zealand’s property market often behaves less like a single national market and more like a collection of regional markets, each influenced by their own local conditions.

Considering an Investment Property?

Understanding how factors like migration, affordability and regional market conditions influence housing demand can be an important part of identifying potential investment opportunities.

At Lighthouse Financial, we guide clients through the investment process and help source high quality property opportunities aligned with their financial situation and long term goals.

If you are considering an investment property, you can get in touch with our team.

If you’d like to learn more, check out the latest property episode on Cheques & Balances.

References

Real Estate Institute of New Zealand (REINZ). (2026). New Zealand Property Report – January 2026.

https://www.reinz.co.nz/libraryviewer?ResourceID=804

Quotable Value (QV). (2026). House Price Index.

https://www.qv.co.nz/price-index/

Lighthouse Financial. (2026). Internal market research and data analysis. Unpublished internal data.

Disclaimer:

The information in this article is general information only, is provided free of charge and does not constitute professional advice. We try to keep the information up to date. However, to the fullest extent permitted by law, we disclaim all warranties, express or implied, in relation to this article – including (without limitation) warranties as to accuracy, completeness and fitness for any particular purpose. Please seek independent advice before acting on any information in this article.