Exploring why property is often considered one of the more effective ways to build wealth, and the role leverage can play in accelerating results.

Looking Beyond Growth and Income

When people talk about property investing, the focus is usually on price growth, rental income, or location.

These are all important factors, and each plays a role in how an investment performs over time. Growth contributes to long-term wealth, income supports holding costs, and location influences both demand and future value.

However, these elements on their own don’t fully explain why property has remained such a widely used approach to building wealth.

Many other asset classes offer growth. Many produce income. Yet property often delivers different outcomes over time.

How to build wealth with property often comes down to more than just growth, income, or location.

A key part of the answer sits behind all of these factors, and is often less understood.

In many cases, investors are not just benefiting from the asset itself, but from the structure around it. They are able to take a position in a larger asset than their initial capital would normally allow, which changes how returns are experienced over time.

That underlying concept is what sits behind many property investment outcomes.

This is leverage.

What Leverage Actually Means

In simple terms, leverage is the ability to use borrowed money to invest.

In property, this usually means contributing a deposit and borrowing the remainder of the purchase price through a mortgage.

This structure allows an investor to control an asset that is significantly larger than their initial capital contribution.

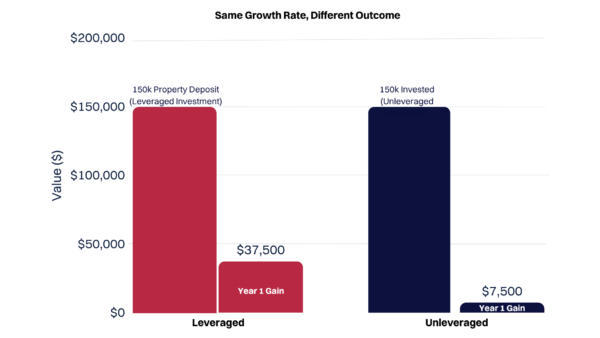

For example, a $150,000 deposit might be used to purchase a $750,000 property, with the remaining $600,000 funded through lending.

Rather than investing $150,000 into an asset worth the same amount, the investor is now exposed to the performance of a much larger asset.

This is a key distinction. The investment itself hasn’t changed, but the scale at which it operates has. Over time, this difference in scale can have a meaningful impact on outcomes.

Why This Changes the Outcome

To put that into context, consider a simple example:

• Property value: $750,000

• Deposit: $150,000

• Loan: $600,000

If that property increases in value by 5%, the gain is $37,500.

Importantly, that increase is based on the full property value, not just the deposit.

If the same $150,000 was invested without leverage, a 5% increase would result in a gain of $7,500.

The rate of growth is the same in both scenarios. What changes is the base that growth is applied to.

This is what gives leverage its impact. It doesn’t increase the growth rate, it increases the exposure to that growth.

Over time, this difference can become more significant, particularly as gains begin to compound.

While the initial capital is the same, the leveraged investment is exposed to a much larger asset, which results in a significantly larger gain from the same rate of growth.

A Simple Comparison: Two Different Approaches

To make this more tangible, consider two investors starting from a similar position.

One investor uses $100,000 as a deposit on an investment property and borrows the remaining funds to purchase a $500,000 asset.

Another investor puts $100,000 into shares, without using leverage.

Assume both investments grow at an average rate of 5% per year.

After one year:

• The leveraged property increases by $25,000

• The share portfolio increases by $5,000

Over time, the difference becomes more noticeable.

After several years, the property investor’s position may also benefit from rental income and gradual loan reduction, increasing overall equity. The share portfolio continues to grow, but only in line with the original capital invested.

This example is simplified, but it highlights how leverage can influence both the scale and pace of outcomes.

How Property Compares to Other Investments

Most investments scale directly with the amount of capital contributed.

When investing in shares, managed funds, or term deposits, returns are typically generated based on the amount invested upfront. Growth and income are tied directly to that initial capital.

Property operates differently.

By using leverage, an investor is able to take a position in a larger asset, which means changes in value apply to a broader base than their initial investment alone.

This doesn’t guarantee stronger performance. However, it does change the way returns are generated and accumulated over time.

It is this structural difference that often sets property apart from other asset classes.

The Compounding Effect Over Time

The impact of leverage is not limited to a single year of growth.

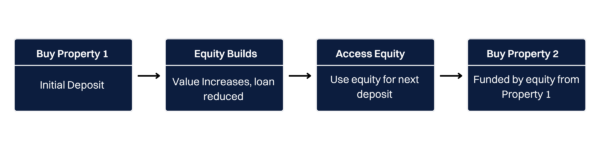

Over time, it can accelerate equity growth as value increases, rental income comes in, and the loan is gradually reduced.

Rental income doesn’t always cover all costs, particularly early on. In some cases, investors contribute a small consistent amount (e.g. $200 a week) to support the investment, depending on rent, interest rates, and how much they’ve borrowed.

As equity builds, it can be accessed and reused to fund additional purchases.

This process can be easier to understand when broken down step by step:

This creates a compounding effect, where investors can build momentum across multiple assets over time.

Understanding “Good” Debt

Not all debt behaves in the same way, and the difference largely comes down to what the debt is used for.

Debt used for consumption typically funds things that do not produce income and often decline in value over time. In these cases, the debt remains, but the asset it was used to purchase does not contribute to long-term financial outcomes.

Debt used for investment can be different.

When linked to a well-selected property, it is connected to an asset that has the potential to grow in value, generate rental income, and be held over the long term. In this context, the debt is part of a broader structure where the asset is working to support the cost of holding it.

The focus shifts from the debt itself to how the underlying asset performs over time.

In practice, this often involves understanding how lending is structured alongside the investment.

A Balanced Perspective

Leverage is not without risk, and it is important to recognise that it can amplify outcomes in both directions.

If property values decline, the impact on equity can be more pronounced. Changes in interest rates can also affect cashflow, particularly in the short term.

In addition, not all properties perform equally. Outcomes are heavily influenced by factors such as location, demand, and asset quality.

For this reason, leverage is most effective when used alongside careful planning, appropriate structure, and a long-term investment horizon.

Understanding both the advantages and the risks is key to using it effectively.

A Familiar Concept, Applied Differently

For many homeowners, leverage is already part of everyday life.

Purchasing a home with a mortgage is, in effect, a leveraged position. Over time, as the property increases in value and the loan is gradually repaid, equity is created.

This process often happens passively, without being actively considered as an investment strategy.

The difference with property investing is not the concept itself, but how it is applied more deliberately.

Rather than being a by-product of home ownership, leverage becomes a tool that can be used to support broader financial goals.

Bringing It Together

Property investing is often discussed in terms of growth and income, but a large part of its effectiveness comes from how those returns interact with borrowed capital.

Leverage allows investors to participate in the performance of a larger asset base, which can influence both the scale and timing of outcomes.

It does not guarantee success, but it does change the structure of the investment in a way that can accelerate progress over time.

Understanding this structure is key to understanding why property can behave differently from other investments.

Final Thought

Leverage is not a new concept, but it is often underutilised or misunderstood in practice.

When applied correctly, it can change not just the return of a single investment, but the pace at which an overall portfolio grows over time.

The key is not simply using leverage, but using it with the right structure and pairing it with the right property. Small differences in asset selection and approach can lead to very different long-term outcomes.

For those considering their next step, the challenge is often less about whether property can work, and more about how to approach it in a way that aligns with their goals.

If you’re looking to build or expand a property portfolio, having the right guidance around both property selection and the overall process can make a meaningful difference. If you’d like help identifying high quality investment opportunities and navigating the process, feel free to get in touch with the Lighthouse Property Team.

If you’d like to learn more, check out the latest property episode on Cheques & Balances.

References

Lighthouse Financial. (2026). Internal market research and data analysis. Unpublished internal data.

Disclaimer:

The information in this article is general information only, is provided free of charge and does not constitute professional advice. We try to keep the information up to date. However, to the fullest extent permitted by law, we disclaim all warranties, express or implied, in relation to this article – including (without limitation) warranties as to accuracy, completeness and fitness for any particular purpose. Please seek independent advice before acting on any information in this article.