If you’re planning to purchase in 2026, whether as a first home buyer or buying an investment property, the key question isn’t just where to buy, but what to buy.

A Supply Wave Is Forming

Apartments, townhouses, and standalone homes are entering very different supply cycles across New Zealand. As the market begins to stabilise and confidence returns, the type of asset you choose may matter more than timing alone.

This is not a one size fits all solution, but a general guide. The right decision will always depend on your individual position, objectives, and risk profile.

Apartments: The Impact of Rising Supply

Apartments often look appealing at first glance. They offer lower entry prices, central locations, and modern finishes. For many buyers, they feel like an accessible starting point.

However, the underlying supply picture is shifting.

Across parts of New Zealand, particularly in larger metropolitan centres, apartment supply has been building in the pipeline.

Using Auckland as a clear example of this trend, apartment completions slowed through 2025, with many projects deferred into 2026 and 2027. That delay has not reduced supply. It has concentrated it.

In Auckland alone, there are 1,104 units currently under construction and a further 2,124 in consent stages targeting 2026 delivery. If those projects proceed, 2026 could exceed the previous cycle peak of 3,133 apartment completions.

That represents a substantial pipeline in New Zealand’s largest city, and Auckland trends often influence broader investor sentiment nationally.

When supply accelerates faster than demand, pricing pressure typically follows. In Auckland, the median apartment price sits at $577,833 in 2025, down 2.42% year on year. Apartments are also forecast to experience the largest increase in suburban supply, not just growth within the CBD.

From a long term performance perspective across New Zealand, apartments have historically tracked around the 3.7% annual growth range. No land ownership, higher density, body corporate costs, and exposure to future supply cycles all contribute to more moderate capital appreciation.

Key takeaways

– For buyers seeking strong capital growth, oversupply can limit performance.

– In a recovery cycle, abundance rarely performs as well as scarcity.

Townhouses: A Balanced Position With Structural Support

Townhouses occupy a strategic middle ground between apartments and standalone homes.

Again using Auckland as a reference point, 888 townhouse building consents were issued in 2025. The median townhouse price sits at $812,167, down 2.53% year on year, reflecting a similar correction to apartments but without the same projected surge in high density supply.

While supply patterns differ across regions, the structural characteristics of townhouses tend to be consistent nationwide.

– Townhouses typically include a land component.

– They operate at lower density than apartments.

– Many avoid complex body corporate structures.

They are also often purchased at a lower entry price than standalone homes, yet can achieve rental levels that are surprisingly similar. That improves yield efficiency, less capital invested for comparable income, while still maintaining exposure to land driven growth.

For owner occupiers, they provide more space without full standalone pricing. For investors, they offer a balance between yield and capital growth.

In a rising market, demand depth becomes critical.

Standalone Homes: Scarcity Remains the Advantage

Land remains the ultimate constraint. You can build upward. You cannot easily create new land in established suburbs.

This principle applies across New Zealand, not just in one city.

Standalone homes are naturally limited by land availability. In markets entering a sustainable expansion phase, properties with meaningful land components have historically outperformed purely vertical stock, particularly when apartment supply is increasing rapidly.

This structural scarcity is one of the reasons standalone homes have historically delivered stronger long term appreciation, typically in the 6.0% range over extended cycles across New Zealand markets.

For buyers focused on long term equity growth, land remains a powerful driver.

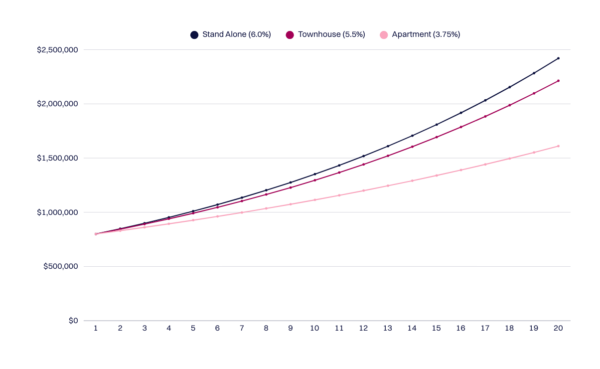

To illustrate how small differences in annual growth compound over time, the chart above models an $800,000 investment across three property types using long-term historical averages: 6.0% for standalone homes, 5.5% for townhouses, and 3.75% for apartments.

By year 10, both standalone homes and townhouses have pulled ahead of apartments. The standalone property grows to approximately $1,351,583 and the townhouse to around $1,295,275, compared to the apartment at roughly $1,114,251. That’s a gap of about $237,000 between standalone and apartment, and around $181,000 between townhouse and apartment in just a decade.

By year 20, the compounding effect becomes significantly more pronounced. The standalone property reaches approximately $2,420,480 and the townhouse around $2,212,518, while the apartment sits near $1,610,141. That places the standalone property more than $810,000 ahead of the apartment, and the townhouse over $600,000 ahead.

These projections are illustrative and based on long-term averages. They don’t account for market cycles, property selection, or standout assets that outperform. The key takeaway is simple: even small differences in annual growth can create substantial gaps in long-term equity.

The Broader Market Outlook: Growth Is Forecast to Return

The wider New Zealand property market is expected to strengthen over the coming years. Stabilised interest rates, improving economic conditions, rising household incomes, and returning buyer confidence all point toward renewed growth.

However, not all property types respond equally when markets recover.

Assets with land value and limited supply constraints tend to lead expansion phases.

Based on long term historical data nationally, standalone homes have typically delivered capital growth in the 6.0% range, largely driven by their larger land component.

Townhouses generally sit just below standalone properties, often tracking in the 5.0 to 5.5% range. While they contain less land than a full standalone property, they still provide exposure to underlying land value that apartments largely lack.

Apartments have historically sat closer to the 4.5% range over long periods.

These differences may seem small annually, but compounded over ten to twenty years, they can create materially different outcomes.

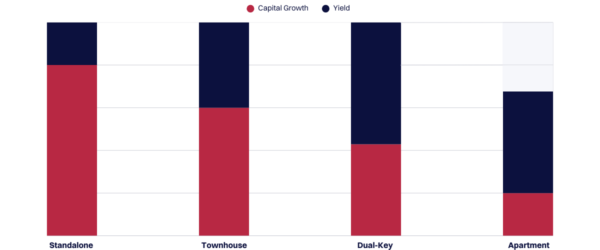

The chart below highlights the structural trade-off between capital growth and yield across different property types.

This graph depicts general trends. There are exceptions to every rule.

So What Should You Buy in 2026?

If growth returns as forecasted, the properties most likely to benefit will typically share a few core characteristics:

– Scarcity

– Underlying land value

– Consistent demand

– Limited risk of oversupply

Right now, apartments in major centres such as Auckland are moving into a concentrated supply cycle. With a large pipeline of stock either under construction or consented, oversupply risk is materially higher in that segment.

By contrast, well located townhouses and standalone homes generally have stronger structural fundamentals heading into the next phase of the market, particularly where land value makes up a meaningful portion of the purchase price.

But this is not a rule book.

Not all property types perform the same way during the same cycle. And more importantly, not every property type suits every buyer.

In 2026, choosing the right asset class may matter more than trying to perfectly time the market, but the right asset depends on:

– Your income and borrowing capacity

– Your risk tolerance

– Whether you’re buying to live in or invest

– Your time horizon

– Your broader financial structure

Most buyers focus heavily on price and location. Fewer step back to analyse supply pipelines, land to value ratios, long term growth drivers, and how a property fits within their wider financial plan.

That’s where clarity matters.

If you’re considering buying, whether it’s your first home, your next home, or an investment property, it’s worth assessing not just what’s available, but what genuinely aligns with your financial position and long term objectives.

At Lighthouse Financial, our property team works alongside you to assess your situation first, then identify opportunities that make sense strategically.

The goal isn’t simply to buy property in 2026. It’s to buy the right property for you.

If you’d like to learn more, check out latest property episode on Cheques and Balances

Reference List

Colliers. (2025). Auckland residential development report 2025.

https://www.colliers.co.nz/en-nz/real-estate-research/auckland-residential-development-report-2025

Lighthouse Financial. (2026). Internal market research and data analysis (unpublished internal data).

Disclaimer:

The information in this article is general information only, is provided free of charge and does not constitute professional advice. We try to keep the information up to date. However, to the fullest extent permitted by law, we disclaim all warranties, express or implied, in relation to this article – including (without limitation) warranties as to accuracy, completeness and fitness for any particular purpose. Please seek independent advice before acting on any information in this article.