Investors aren’t always waiting to save another deposit. How equity is being used to move sooner, and when it works.

Rethinking the Starting Point

Most people assume buying an investment property means starting again.

Another deposit. Another few years of saving. Then maybe, you can look at investing.

But that is not always how it plays out.

A growing number of homeowners are not waiting to rebuild a deposit from scratch. Instead, they are using the position they have already built in their existing home.

That usually comes down to one thing. Equity.

If you have owned your home for a few years, you have likely paid down some of your mortgage while the property may have increased in value. Both of these build equity over time.

Understanding Equity vs Usable Equity

One point that often gets missed is the difference between equity and usable equity.

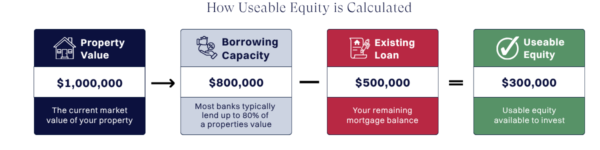

Equity is what you own in the property. If your home is worth $1,000,000 and you owe $500,000, you have $500,000 in equity.

But you cannot access all of that.

Banks will usually cap lending at around 80 percent of the property’s value. As you can see in the visual below, that means total lending can go up to $800,000 on a $1,000,000 property.

With an existing loan of $500,000, that leaves $300,000 as usable equity.

That is the portion that can actually be drawn on and used.

Turning Equity into a Deposit

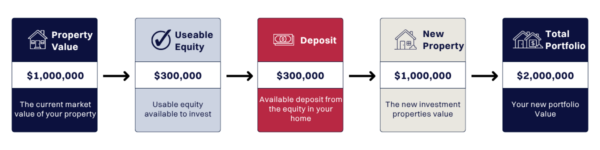

This is typically how the deposit is funded.

Rather than saving $200,000 in cash, the same amount is secured against your existing home. The bank uses that property as security, and the new investment property becomes security for the remaining lending.

From a practical point of view, this brings the timeline forward.

Instead of waiting several years to build another deposit, some homeowners are able to move based on what they already have.

This is often described as buying with “no cash deposit”. The deposit still exists, it is just structured differently.

From Equity to Purchasing Power

This approach is more common than people expect.

Most investors are not repeatedly saving deposits in cash. They are using equity as they go. That does not mean it is always the right move, but it does explain why some people are able to enter the market sooner.

The equity itself is not what you are buying with. It is what unlocks the ability to borrow.

For example, $200,000 in usable equity can support a purchase of up to $1,000,000 if a 20 percent deposit is required.

The equity covers the deposit, and the remaining lending sits against the new property.

The Cash Flow Reality

Using equity increases your total debt.

That typically means higher repayments compared to using a large cash deposit.

As a simple example, a property renting for $650 per week might cost $750 to $800 per week to hold once lending and expenses are included.

That leaves a shortfall that needs to be covered from income.

The size of that gap will vary, but it is usually part of the structure rather than a short-term issue.

Leverage and Timing

The reason this approach is used comes down to leverage.

Returns are based on the value of the asset, not just the cash invested upfront. If you buy a $700,000 property and it increases by 5 percent, that is a $35,000 gain.

Where equity becomes relevant is timing. It allows some investors to enter the market earlier, rather than waiting to rebuild a deposit.

If you want a deeper explanation of how leverage works in practice, you can read more here.

Risk and Lending Limits

Leverage does not only amplify gains.

If prices are flat or fall, your debt remains the same and your costs continue.

There is also the bank’s servicing assessment. Even with sufficient equity, you still need to show that you can afford the additional lending under test rates.

In many cases, servicing becomes the limiting factor rather than equity itself.

Bringing it Back to Real Situations

Using equity is not a shortcut. It is a different way of structuring the investment.

You are reducing the need for upfront savings, but increasing your exposure to debt and cash flow.

Across New Zealand, it is common to see homeowners who have held property for several years sitting on usable equity.

Often, the assumption is that investing requires starting again from zero.

In reality, the ability to invest is often already there. The decision is whether the structure works.

Final Thoughts

Using equity is one of the more common ways people enter the investment property market in New Zealand.

It can allow you to move forward without waiting years to save another deposit, particularly if you already have a strong equity position.

Like any strategy, it works best when it is well understood and structured carefully.

If you already own a home, you may be closer to investing than you think. If you want to understand how much usable equity you have and what that could translate to, feel free to get in touch with the Lighthouse Property Team.

If you’d like to learn more, check out the latest property episode on Cheques & Balances.

Disclaimer:

The information in this article is general information only, is provided free of charge and does not constitute professional advice. We try to keep the information up to date. However, to the fullest extent permitted by law, we disclaim all warranties, express or implied, in relation to this article – including (without limitation) warranties as to accuracy, completeness and fitness for any particular purpose. Please seek independent advice before acting on any information in this article.