Most people don’t think about life insurance because they expect life to unfold as planned - the mortgage gets paid down, the kids grow up, and everything falls into place.

Life insurance is there for the moments that don’t. This guide helps you work through what your family would need to maintain their lifestyle and cover key costs if the unexpected happens.

Disclaimer

While this resource is a helpful one-pager, we recommend speaking with an Insurance Adviser to ensure you’re not missing any crucial information when calculating the right level of cover.

An Insurance Adviser does not charge a fee. They will recommend the appropriate levels of cover, the right provider, and work to secure the best possible terms – including for any pre-existing conditions.

If you’d like to speak with an Insurance Adviser, you can click here to receive a personalised Statement of Advice at no cost.

Life Insurance Calculation

The purpose of life insurance is to ensure your family can maintain their lifestyle if you were to pass away unexpectedly.

If you do not have dependants, you may not need life insurance. Instead, you may wish to explore income protection or health insurance. You can find more information here.

The key areas to consider when calculating life insurance are:

– Debt repayment

– Time off work for a spouse or partner

– Replacement income

– Children

– Funeral and estate costs

– Other considerations

Debt Repayment

How much is your mortgage?

Can your spouse or partner afford to maintain the current mortgage and other expenses?

If not, what size mortgage could they realistically manage?

Calculate total:

Tip: If you and your partner earn similar incomes, some choose to clear half the mortgage so contributions remain broadly equal.

Time Off Work

If you passed away, it would be an incredibly difficult time for your family. The last thing most people want to do is rush back to work.

Some choose to allocate a lump sum through life insurance to allow their spouse or partner time away from work.

– Would you like to allocate life insurance for this purpose?

– If yes, what is your spouse or partner’s after-tax monthly income?

– How many months would they like to take off work?

Calculate total:

Replacement Income

– What are your household expenses per month?

– If you passed away, what would the household income be after tax?

– Is there a shortfall?

– If yes, how much is the deficit per month?

– For how many years would you like to cover this deficit?

Calculate total:

Tips: If your mortgage has been repaid, remember your household expenses will reduce.

Many clients choose to cover five years, or until their youngest child turns 18, though this varies case by case.

Children

If you have children, you may wish to set aside a lump sum to support them. Common considerations include:

– Would there be additional costs such as a cleaner, nanny, or childcare?

– If yes, what is the annual cost and how many years would support be needed?

– Do you need to cover private school fees? What is the total cost?

– Would you like to set aside a lump sum for university fees?

– Would you like to set aside a lump sum for a first home deposit?

Calculate total:

Funeral and Estate Costs

Tip: Typical costs range from $15,000 to $50,000.

Other Considerations

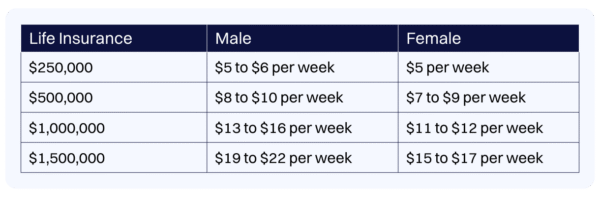

How Much Does Life Insurance Cost? (As at July 2025)

35-year-old healthy non-smoker

Disclaimer

These prices are indicative only and not guaranteed. Premiums can change, and your health may affect pricing.

The figures above are retail rates. Our Advisers can often restructure policies to better fit your budget.

Why Talk to an Insurance Adviser?

Right Levels of Cover

Our Insurance Advisers will meet with you to understand your situation and the risks facing you and your family.

They’ll explain the different types of insurance, recommend the right level of cover, and ensure it fits within your budget.

Right Provider

We work with all the leading life and health insurance providers in New Zealand. Each provider offers different features, benefits, and pricing depending on age, gender, and cover levels.

Underwriting

There are two sides to insurance: you want cover, and the insurer wants to understand your risk.

It’s common for policies to include exclusions or loadings due to past health issues, whether large or small.

Your Adviser will help complete your application accurately and work across the market to secure the best possible terms.

Reviewing Your Cover

Your insurance recommendation is right for you at that point in time – but life changes.

Buying a home, having children, receiving a pay rise, or paying down debt can all affect your insurance needs.

Your Adviser will review your cover annually to ensure it remains appropriate.

Claims Support

We hope you never need to claim on your insurance.

However, if the time comes, having the right support matters. Your Adviser will be your first point of contact and will guide you through the claims process every step of the way.

Why a Lighthouse Insurance Adviser?

Our Insurance Advisers live and breathe insurance. They’re passionate about delivering an exceptional client experience and understand insurance inside and out.

We also take a holistic view of your financial plan. Every dollar spent on insurance is a dollar not going toward debt reduction or investing.

Our ultimate goal is to help you build wealth over time, achieve financial freedom, and eventually reduce or cancel insurance when it’s no longer needed.

Need to Review Your Insurance?

Get in touch with the Lighthouse Insurance team for a personalised Statement of Advice at no cost.

If you’d like to learn more, follow our clients Dion and Rachel’s insurance journey.

Disclaimer:

The information in this article is general information only, is provided free of charge and does not constitute professional advice. We try to keep the information up to date. However, to the fullest extent permitted by law, we disclaim all warranties, express or implied, in relation to this article – including (without limitation) warranties as to accuracy, completeness and fitness for any particular purpose. Please seek independent advice before acting on any information in this article.