A closer look at how houses and townhouses compare across capital growth, cashflow and affordability, and why the “better” investment depends on more than just land.

The Assumption Most Investors Start With

Most new property investors begin with a simple assumption. Standalone houses are the better investment.

It seems logical. Houses come with land, and land is often seen as the driver of long-term value. Scarcity, redevelopment potential, and past performance all tend to support that view.

But when you look more closely at how different property types have actually performed, the answer is not as clear as it first appears.

Two Assets, Different Starting Points

When comparing houses and townhouses as investments, the key differences are less about who buys them, and more about how they are priced and how they perform financially.

Standalone houses typically come with higher entry prices and a larger land component. Townhouses tend to sit at lower price points and are more accessible from a borrowing perspective.

From an investment point of view, this difference in entry price has a direct impact on leverage, cashflow, and how easy a property is to hold over time.

Rather than thinking about them as completely different markets, it is more useful to think of them as different ways to access the same market, but with different financial characteristics.

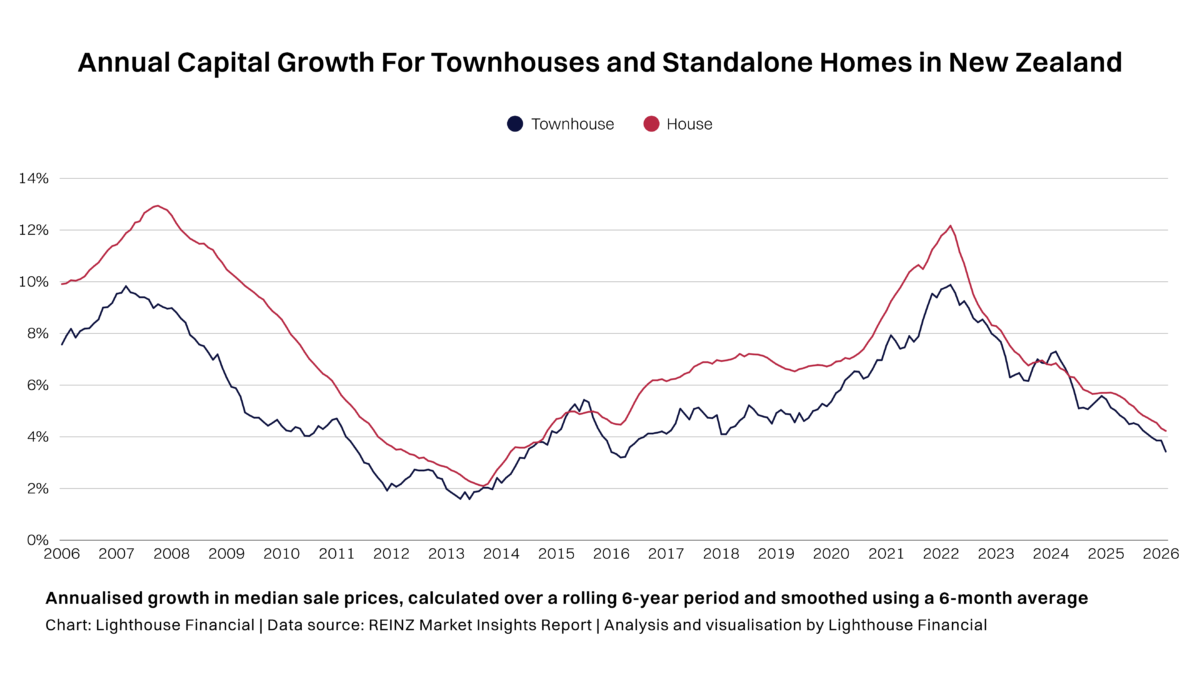

Capital Growth: Closer Than Most Expect

When you look at the data over time, both houses and townhouses tend to follow very similar patterns.

As shown in the chart above, periods of strong growth, slowdowns, and recoveries are largely aligned. The overall direction of the market impacts both asset types in a similar way.

Houses do track slightly higher in terms of capital growth. However, the gap is relatively small when viewed across a full cycle.

The more important point is that both asset types are being driven by the same underlying forces. They tend to rise and fall together, rather than behaving as completely separate markets.

Why Townhouses Hold Up Better Than Expected

A key reason townhouses perform more closely to houses comes down to the relationship between price and rent.

In many cases, townhouses are a fair bit cheaper to purchase, but do not give up much in terms of rental income. Houses may achieve slightly stronger capital growth over time, but townhouses often deliver slightly stronger yields as a result of the lower entry price.

This creates a more balanced outcome than many investors expect. You are not necessarily sacrificing much income, despite a meaningful difference in purchase price.

Another factor is that most townhouses still have a land component, just in a smaller proportion. This means they are not completely detached from the land-driven dynamics that support house prices over time.

Affordability continues to support demand. As prices rise, more buyers are pushed towards lower entry points, which helps maintain consistent interest in attached housing.

Lower price points also improve liquidity. Townhouses tend to be easier to transact, which can support price stability during softer market conditions.

Where Houses Still Have An Edge

Despite the similarities, houses do retain some structural advantages.

The land component remains important, particularly over longer timeframes. In established suburbs where land is limited, standalone properties can benefit from stronger underlying scarcity.

There is also the potential for redevelopment or intensification, which can add another layer of value in certain locations.

These factors mean houses may still have an edge in specific contexts, particularly where land is tightly held and supply is constrained.

Cashflow And Affordability Change The Equation

While capital growth often gets the most attention, cashflow and affordability can have a significant impact on investment outcomes.

Townhouses generally have lower entry prices, which reduces the amount of debt required to purchase. At the same time, rents are often not dramatically different for comparable properties in similar locations.

This means that, in many cases, townhouses can offer stronger yields relative to their purchase price.

Put simply, you are often paying significantly less to buy the property, without giving up much in terms of rental income.

Even small differences in yield or purchase price can materially affect how easy a property is to hold over time. This becomes particularly important in higher interest rate environments.

Houses, with higher entry prices, often require a larger financial commitment. While they may offer long-term advantages through land exposure, the short-term cashflow profile can be more demanding.

If you have recent Auckland or Christchurch figures for typical purchase prices, rents, and yields for each asset type, this is a good place to reference them briefly to ground the comparison.

A Simple Way To Think About It

“The better investment depends less on the property, and more on the investor.”

This is where the comparison tends to shift.

Rather than asking which asset type is better in isolation, it is often more useful to consider what each one allows an investor to do. Entry price, holding cost, and access to finance all influence what is practical.

In many cases, the decision is shaped less by preference and more by situation.

The Better Investment Depends On The Investor

When you bring these factors together, the idea of a single “better” investment becomes less clear.

Houses offer stronger exposure to land and may benefit from scarcity over time. Townhouses provide more accessible entry points, broader demand, and often more manageable cashflow.

The right choice depends on the investor’s position, including budget, risk tolerance, and long-term goals.

Rather than focusing on which asset type is better, it is often more useful to understand the trade-offs and how each option fits within a broader investment strategy.

Like any strategy, it works best when it is well understood and structured carefully.

If you want to understand what is best for your situation, feel free to get in touch with the Lighthouse Property Team.

If you’d like to learn more, check out the latest property episode on Cheques & Balances.

Disclaimer:

The information in this article is general information only, is provided free of charge and does not constitute professional advice. We try to keep the information up to date. However, to the fullest extent permitted by law, we disclaim all warranties, express or implied, in relation to this article – including (without limitation) warranties as to accuracy, completeness and fitness for any particular purpose. Please seek independent advice before acting on any information in this article.